Age of Controversy

How global organizations respond to tax disputes today

Foreword

In a global tax system that values tax transparency, and with governments under pressure to balance public finances, it is unsurprising that organizations are seeing rising numbers of tax controversies. With a tax controversy increasingly involving multiple jurisdictions, it also takes longer to reach resolution.

As a result, responding appropriately to tax controversy is a strategic priority for organizations. This often drives a more proactive, open approach to voluntary disclosures and information sharing with tax authorities. It has also led organizations to hire dedicated in-house resource to respond to controversy. Indeed, this survey shows that in the past three years a majority of businesses have hired this dedicated resource at both local and global levels.

Foreword by:

Nonetheless, organizations still look for an external perspective at key moments. Sometimes that is at a procedural tipping point, sometimes it is when the potential financial and reputational impact of the controversy becomes clearer and sometimes it is due to stakeholder anxiety at board or shareholder level. As this survey shows, when seeking external support organizations want to engage with those with a track record of handling similar matters for similar organizations with the same tax authority.

Experience and insight matter in resolving a controversy, therefore, and so does keeping options open. While survey respondents noted that public litigation isn’t necessarily the first choice to resolving a tax controversy, litigation skills and experience can still be a highly effective part of the strategy in reaching a non-litigious settlement. This twin-track approach delivers effective and robust settlements and gives peace of mind that actions taken today remain appropriate should the controversy escalate.

Finally, a couple of broader points. The first is that the professionalization of tax controversy within organizations is not an attack on the tax system. The interviews carried out alongside the survey demonstrated clear respect both at a local and global level for a fair and functioning tax system. Both interviewees and survey respondents were in fact interested in closer relationships with tax authorities where possible. However, there was a measure of frustration at the difficulties of interpreting cross-border policies at a local level and a recognition that the uncertainty arising from this is a likely driver of future tax controversy.

Secondly, with controversy now a regular experience, responding to controversy should be part of wider business governance. This includes updated risk registers, policies on data retention and sharing that consider potential future controversies, clear local and regional/global stakeholders for responding to controversy and decision trees for handling controversy that unite board level commitments on tax transparency with timely and appropriate actions during a controversy.

In summary, organizations are experiencing greater levels of tax controversy and this trend is unlikely to reverse soon. This survey provides rich data on the impact of tax controversy on international and fast-growing organizations, alongside clear trends on how organizations are responding to the challenge.

Introduction

Globally, several forces are at work that complicate and increase the time needed to manage tax affairs: legislators are adding new layers to national and international tax codes; revenue agencies are challenging tax filings by large and fast-growing businesses and are more willing to co-operate across borders; and environmental, social, and governance (ESG) concerns have the public and shareholders demanding transparency and accountability.

This will almost certainly mean that the current high levels of tax controversy will endure for the foreseeable future as companies struggle to digest complex new legislation and tax authorities remain emboldened to raise more enquiries, due both to the public appetite for tax transparency and to recent events. The financial repercussions of the COVID-19 pandemic are widely understood to have pressured tax authorities to both scrutinise tax credits and subsidies granted during the crisis and help refill public coffers.

In response to this controversy landscape, many companies have expanded their internal resources, appointing specialist managers at a senior grade with direct responsibility for controversy management, and making tax departments an integrated part of the strategic risk management function.

But what does good practice look like for these new heads of controversy? To assess how businesses are responding to rising tax controversy, Deloitte asked International Tax Review (ITR) to survey more than 300 companies across all major sectors, with annual revenues from under $500 million to above $5 billion. Just over half are listed, while C-suite comprised the biggest group of respondents, mostly from tax, finance and legal departments.

We also wanted to understand how regional differences affect corporate tax policy, so the survey was split evenly between companies headquartered in the Americas, Europe, Asia-Pacific, and the Middle East and Africa. For further insight into regional and sectoral variation, we conducted in-depth interviews with key tax decision-makers across the corporate world.

Our goal is to illuminate the most frequent areas for controversy, how companies formulate responses and what drives their decision-making. The result is clear and consistent data at a global level, along with some startling regional insights.

For instance, there is broad agreement that tax disputes are escalating globally, are taking longer to resolve and require specialist external support, but there are clear regional trends in which topics attract controversy and how many disputes occur. Regions also differ in how recently companies have built dedicated internal resources for handling controversy, the point at which they seek external advice and their rationale for when and whether to challenge revenue authorities.

This survey concludes with a short summary of what best practice might look like in the new age of controversy.

Tax disputes are increasing at a global level, according to 77% of respondents, with financing arrangements and residency matters being the most troublesome issues.

Scrutiny of low-tax jurisdictions is another prime driver of controversy – at both global and domestic level – while US respondents called out a rise in conversations around digital service taxes.

Companies are beefing up internal resources, with 78% creating or planning to create dedicated senior management to oversee tax disputes.

In disputes, companies are more fearful of the reaction from shareholders than from tax authorities.

Most companies prefer to get input from external advisors on their tax disputes, with over three quarters finding an independent outside perspective usually or always useful.

Furthermore, a supportive second review is key to a company’s confidence in challenging a tax authority.

Rapid outsourcing reaps rewards. Asia-Pacific companies are most likely to involve advisors at the start of disputes and are also most satisfied with external tax advice.

Some 70% said it is almost always useful, roughly double the proportion of North American and European firms.

The larger the company, the more influence its tax department has on hiring external advisors.

Most (52%) of those with revenues exceeding $5 billion delegate this decision to the tax team, versus only 25% among sub-$500 million companies, where the finance department holds sway. Furthermore, the specialists appear to appreciate an external perspective, as satisfaction with external advisors generally increases with company size.

“I would be extremely surprised if tax disputes did not skyrocket in the upcoming years due to the amount of new legislation and especially to its great complexity and need for coordination between a huge amount of jurisdictions,” said Jaime Salmerón, Regional Tax Lead Benelux & EU Tax Policy and CFO Netherlands Office for oil company Repsol.

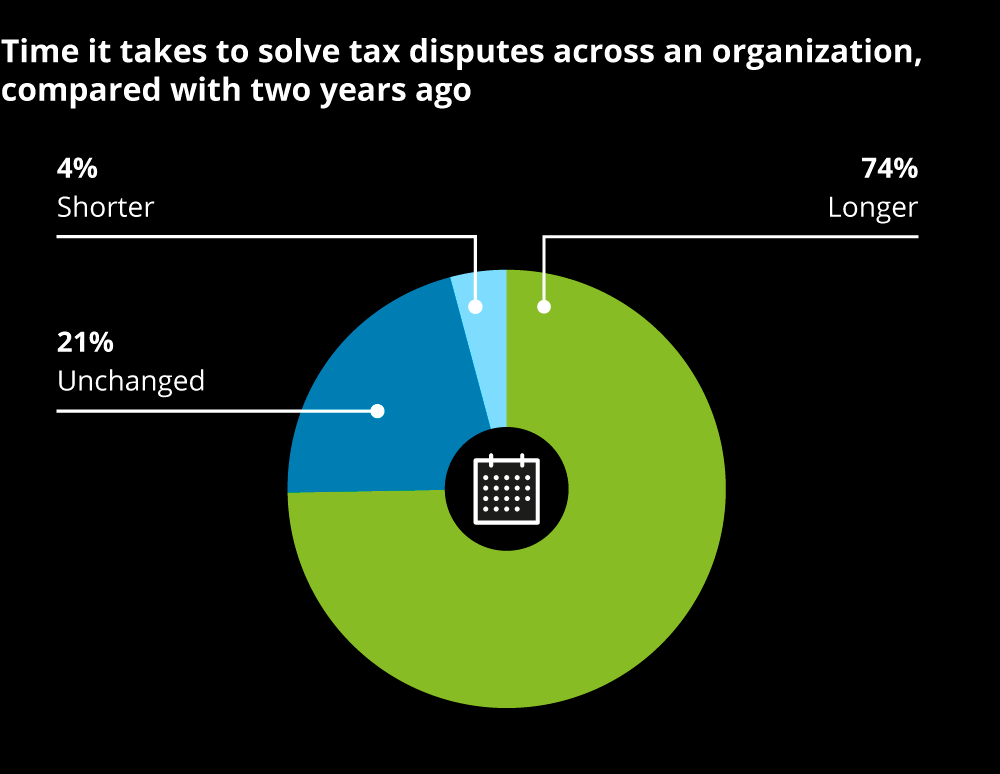

Already, tax disputes are escalating across multinational operations. Almost every North American company in our survey has observed a rise in the past two years, as have a big majority of those from each of the other regions. Furthermore, three-quarters of all respondents said that their global disputes are taking longer to resolve.

The increased levels could reflect the fact that tax controversies frequently involve multiple jurisdictions, albeit there are some regional variations in how strongly this has impacted businesses. Sixty percent of companies have run into cross-border collaboration between revenue authorities. More than three-quarters of North American respondents have experienced an enquiry from their local authority on behalf of a foreign one, versus 37% of Asia-Pacific-headquartered companies.

Furthermore, almost every (94%) North American respondent has experienced a tax dispute involving multiple revenue authorities in relation to the same issue in multiple jurisdictions, versus 60% of European companies and a global average of 73%.

“In many cases nowadays you have to engage with more than two tax authorities at the same time, with the same transaction,” said Sanna Jäälinoja, Group Head of Transfer Pricing for Finnish stainless steel producer Outokumpu.

Despite these global trends, there are clear regional differences in terms of what issue might trigger a tax controversy. The rise in global controversy is being driven by questions about financing arrangements and residency matters, followed by scrutiny of low-tax jurisdictions, which is the most common cause of extra controversy at a domestic level, according to the survey.

However, in North America and in Asia-Pacific, the leading drivers for tax controversy are the digital services tax and financing arrangements, respectively. As can be seen, the topics that businesses identified as being the subject of controversy fall within the most complex areas of the global and domestic tax codes.

Salmerón noted: “In the last 10 years the tax landscape has changed a lot. There have been a lot of developments, a lot of new regulations – things are getting far more complex.” Plus, he added, the public is paying more attention. “There is a huge appetite for more transparency from media, from stakeholders, from individuals.”

Some of this complexity stems from new international regulations such as the OECD’s Base Erosion and Profit Shifting (BEPS) project. Ahead of implementation of the BEPS Inclusive Framework in 2023, companies are racing to understand the new rules – and how different tax authorities may interpret them.

While businesses respect and accept the global tax framework in which they must now operate, the complexities of implementing what is essentially international policy-making within existing domestic legislation is expected to drive uncertainty that may ultimately only be resolved through tax controversy between businesses and tax authorities.

At Repsol, Salmerón noted the challenges involved in incorporating the OECD rules into European Union law, and the wider issue of interpretation discrepancies. “How will different countries understand these rules should apply? It could create a huge mess in the sense that you have different interpretations.”

In addition to ongoing tax changes, businesses also point to the repercussions of the coronavirus pandemic.

“During the COVID years, finance ministries provided a lot of subsidies but now they are entering a phase where they need to ensure collection of their revenues,” observed Laura Greco, Head of Tax for Vodafone Italia. “So I expect them to tighten their monitoring of the eligibility for the tax incentives and tax credits that have been accessed by multinationals.”

Given the growing volume, duration and complexity of tax disputes, the ability to resolve them either pre-emptively or through a formal challenge has become a strategic priority.

“In the past the tax department was part of the administration of the finance operation. Now tax is considered as a risk function and it has a more strategic role. Now all the people I have in my team are very senior, with at least 25 years of experience,” said Greco, adding that Vodafone Italia’s internal tax resources have roughly doubled in the past five years.

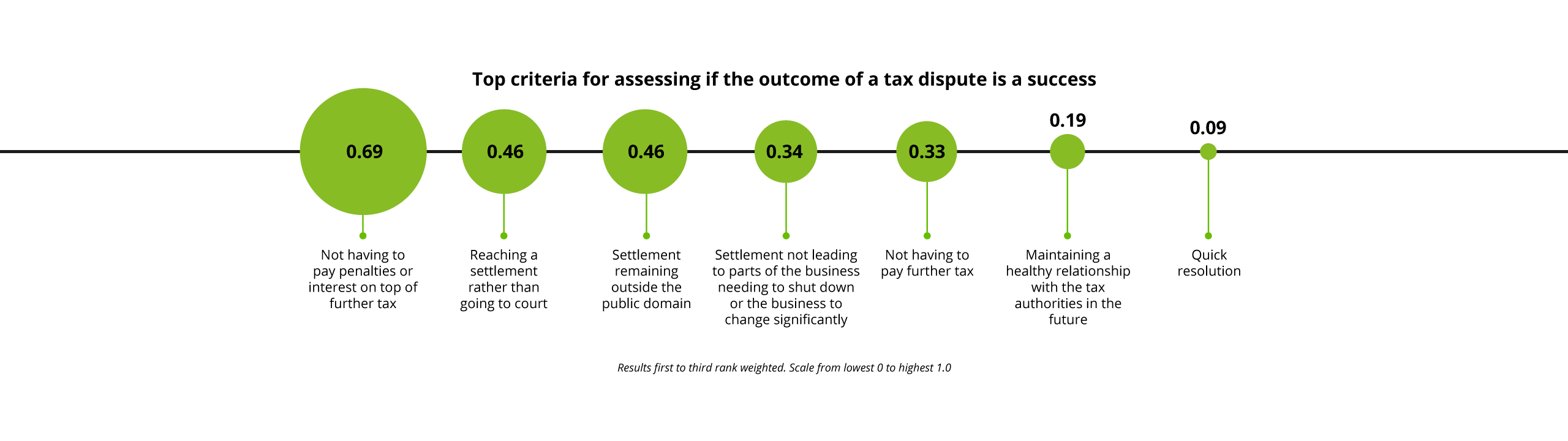

The pressures outlined above mean that companies must work harder to achieve the key outcomes they want from a dispute. Avoiding penalties or additional interest is by far the most important, shows the survey, followed by reaching a settlement outside the public domain.

Keeping senior management in the loop

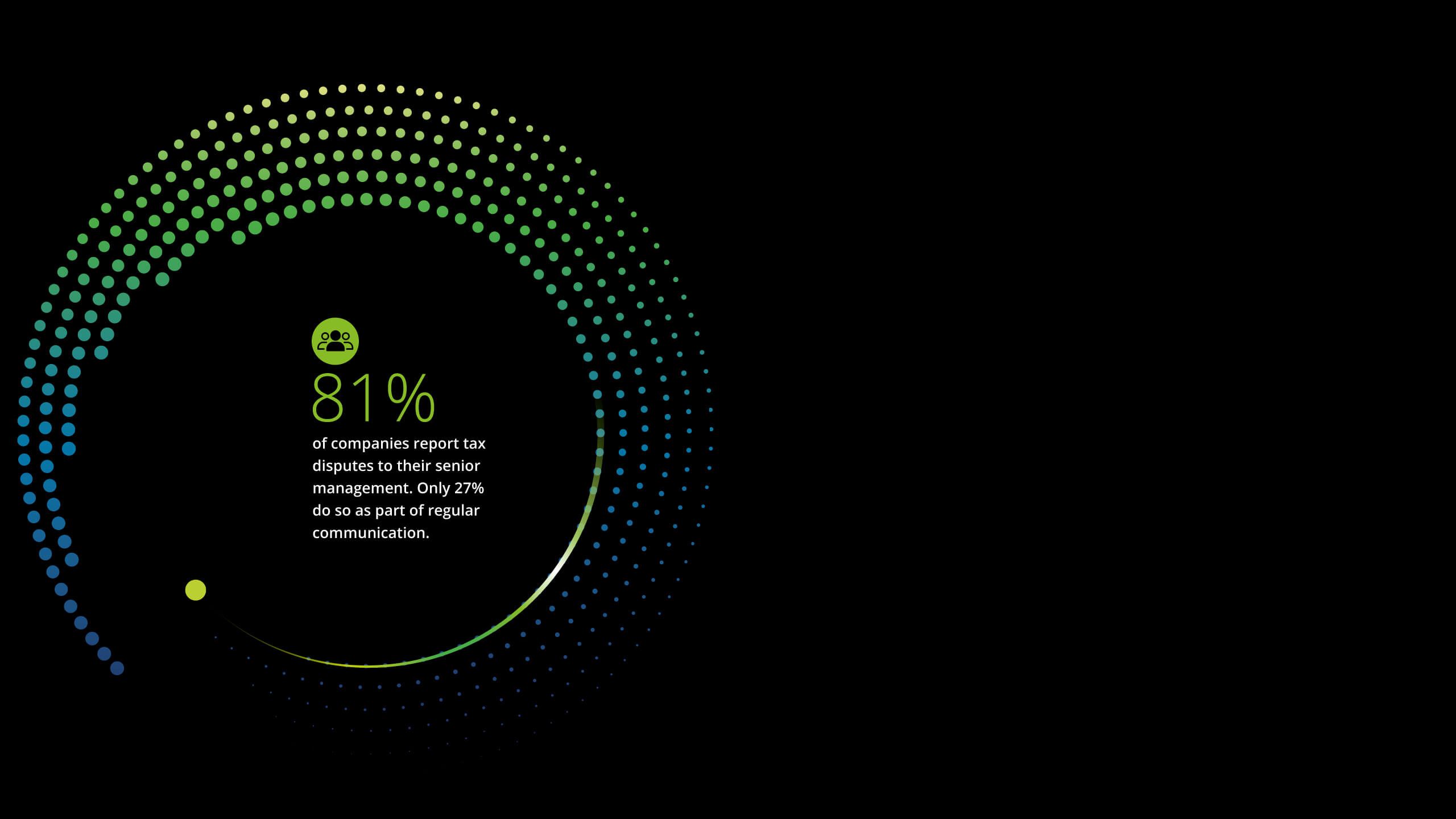

At present, a large majority of companies (81%) report tax disputes to their senior management, although only 27% do so as part of regular communication. The point at which that reporting happens also varies, with almost a third doing so when a tax liability arises and 11% upon entering litigation.

“It is a good practice to keep senior management in the loop on all significant tax matters. In select cases, it may also be advisable to keep board and investors updated,” noted Haroon Qureshi, Vice-President Taxes for business services provider Genpact.

Again, the global statistics hide regional variations in corporate policy. While almost half (53%) of Latin American companies inform senior management of tax disputes as a matter of course, an almost equal share (51%) of Asia-Pacific respondents only do so when a liability arises, and a further 23% only when litigation occurs.

A complex mix of how aggressive local tax authorities are, and how confident companies are in their own and their advisors’ ability to handle a dispute effectively up until certain tipping points may explain those regional variations. Differences in corporate governance structures may also play a role.

Roles and responsibilities

In response to the growing volume of tax disputes most companies (63%) already have a specialized role such as VP Tax Controversy, with 38% of those having created this position more than three years ago. Only 22% of companies in our survey did not see a need for it.

Dedicated resources on payroll mean that 42% of companies tend to handle tax controversy internally, and a big majority have processes in place to report disputes up the chain of command.

“In countries in which we don't have expertise, we rely on advisors,” said Salmerón. “But we also have local tax teams in the countries in which we are strong.”

Indeed, good tax oversight begins at home. Effective risk management hinges on the flow of up-to-date and regular information and that applies during a controversy as well as during business as usual.

“Tax cannot do its job without information about what the business is doing, and you can only have access to that information if you are close to the business,” observed Greco at Vodafone Italia, who added that nowadays tax can be seen as part of a business’s risk management function.

A key role for tax teams and any VP of Controversy is having visibility on where there are open controversies at regional and global levels, what stage they are at and when and how a decision point has been reached. One of those decision points is when to seek external support.

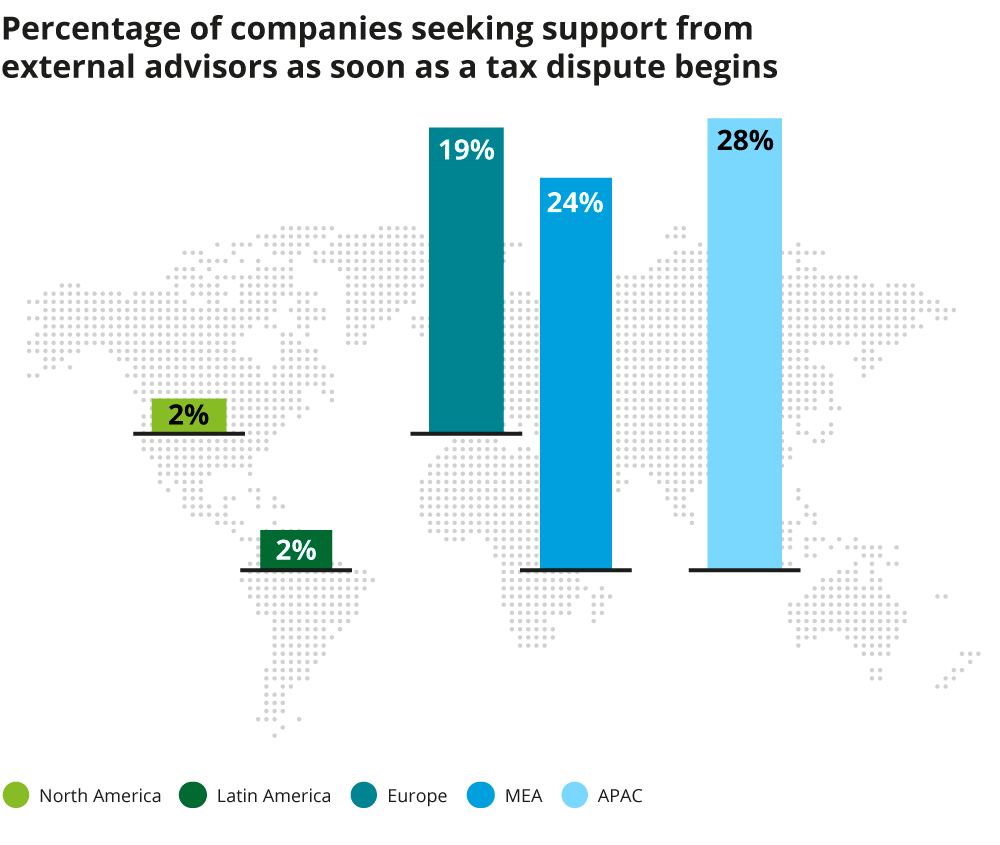

Asia-Pacific companies are the quickest to reach for external support, with 28% calling in advisors as soon as a dispute begins, whereas North America is the region that tends to rely most heavily on internal resources. Interestingly, size of organization is less of a factor here. As a matter of course, 30% of businesses with revenues above $5 billion like to supplement their analysis with an independent opinion, hiring external advisors as soon as controversy arises.

Alongside the need for a VP of Controversy or Head of Tax to communicate with their internal stakeholders, the relationship with a tax authority is obviously crucial to reaching resolution. Accordingly, two-thirds of companies desire more frequent contact with the authority during a dispute.

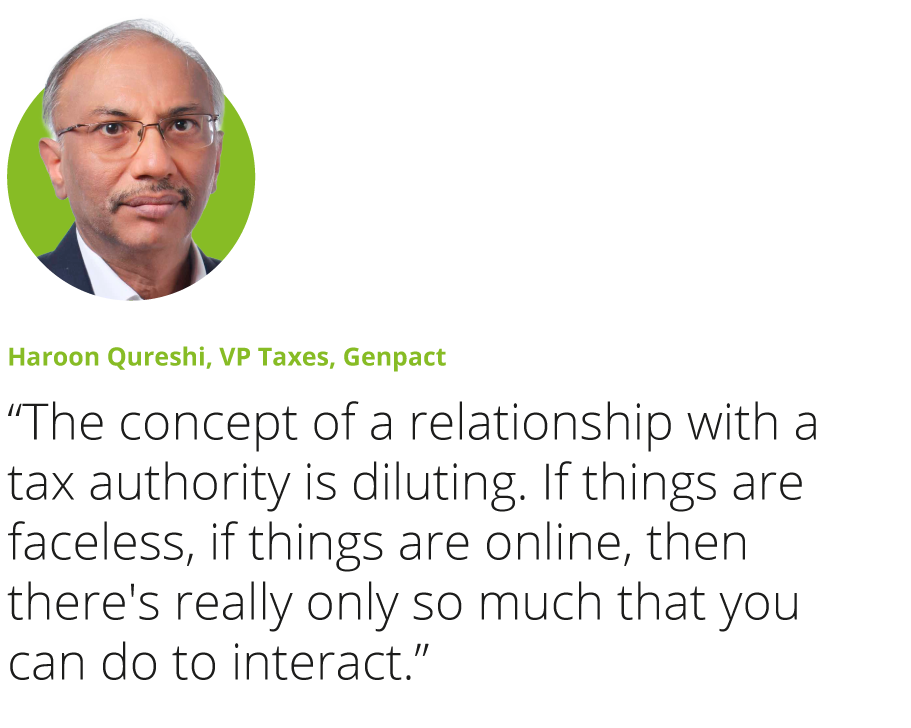

It’s an issue that is becoming increasingly complex, according to Qureshi. Using the example of India, he observed that digitization of tax reporting and auditing has cut into opportunities for face-to-face discussions with revenue officials.

“The concept of a relationship with a tax authority is diluting. If things are faceless, if things are online, then there's really only so much that you can do to interact,” he said.

This is important because without the opportunity for organizations to explain crucial context and detail around key tax and finance decisions, the potential for misunderstandings to persist during a controversy rises. In addition, the longer that misunderstandings or misperceptions continue the more likely it is that both sides in a controversy harden their positions, frustrated that the other party ‘doesn’t get it’ and isn’t co-operating with the process.

Roles and responsibilities

In response to the growing volume of tax disputes most companies (63%) already have a specialized role such as VP Tax Controversy, with 38% of those having created this position more than three years ago. Only 22% of companies in our survey did not see a need for it.

Dedicated resources on payroll mean that 42% of companies tend to handle tax controversy internally, and a big majority have processes in place to report disputes up the chain of command.

“In countries in which we don't have expertise, we rely on advisors,” said Salmerón. “But we also have local tax teams in the countries in which we are strong.”

Indeed, good tax oversight begins at home. Effective risk management hinges on the flow of up-to-date and regular information and that applies during a controversy as well as during business as usual.

“Tax cannot do its job without information about what the business is doing, and you can only have access to that information if you are close to the business,” observed Greco at Vodafone Italia, who added that nowadays tax can be seen as part of a business’s risk management function.

A key role for tax teams and any VP of Controversy is having visibility on where there are open controversies at regional and global levels, what stage they are at and when and how a decision point has been reached. One of those decision points is when to seek external support.

Asia-Pacific companies are the quickest to reach for external support, with 28% calling in advisors as soon as a dispute begins, whereas North America is the region that tends to rely most heavily on internal resources. Interestingly, size of organization is less of a factor here. As a matter of course, 30% of businesses with revenues above $5 billion like to supplement their analysis with an independent opinion, hiring external advisors as soon as controversy arises.

Alongside the need for a VP of Controversy or Head of Tax to communicate with their internal stakeholders, the relationship with a tax authority is obviously crucial to reaching resolution. Accordingly, two-thirds of companies desire more frequent contact with the authority during a dispute.

It’s an issue that is becoming increasingly complex, according to Qureshi. Using the example of India, he observed that digitization of tax reporting and auditing has cut into opportunities for face-to-face discussions with revenue officials.

“The concept of a relationship with a tax authority is diluting. If things are faceless, if things are online, then there's really only so much that you can do to interact,” he said.

This is important because without the opportunity for organizations to explain crucial context and detail around key tax and finance decisions, the potential for misunderstandings to persist during a controversy rises. In addition, the longer that misunderstandings or misperceptions continue the more likely it is that both sides in a controversy harden their positions, frustrated that the other party ‘doesn’t get it’ and isn’t co-operating with the process.

Fearing retaliation?

Despite the potential for frustrations and misunderstandings to arise in a tax controversy, this doesn’t translate into organizations fearing tax authority retaliation in the longer term as a result of how a dispute resolves. Instead, outside the Americas, companies appear to worry more about the impact of a tax dispute on shareholder relationships. Some 57% of companies from Europe, the Middle East and Africa fear negative reactions from shareholders due to a tax dispute, but less than a third (32%) are similarly concerned about a tax authority’s response.

“Tax is increasingly a topic of interest to shareholders and the public,” noted Outokumpu's Jäälinoja. “In addition, the importance of sustainability and ESG topics is increasing significantly, therefore additional transparency is required and the requirements increasingly come from outside tax rules and regulations.”

And while tax authority retaliation is just about the main concern of companies from the Americas, only 11% of Asia-Pacific companies worry about it. Furthermore, half of them never worry about any form of retaliation.

Despite this confidence, companies based in Asia-Pacific don’t appear significantly more assertive when controversy arises. Of 61 companies interviewed in the region, 36% stressed that they are willing to challenge a tax authority’s position and 61% said they are sometimes willing, versus respective figures of 32% and 66% for the global survey. The confidence shown in Asia-Pacific about lack of tax authority retaliation may demonstrate a higher level of trust in how the tax system functions compared with other regions, which reduces the feeling that there is a need to strongly challenge tax authorities during a controversy.

INVESTOR'S VIEW:

“Interest in tax transparency will rise”

Kate Elliot, Head of Ethical, Sustainable and Impact Research at Rathbone Greenbank Investments, the ESG-focused team within wealth manager Rathbones Group, discussed how investors shape the tax transparency agenda.

“One topic frequently raised by clients is the concept of tax justice and the view that all participants in an economy should contribute towards the public goods that enable that economy to function, be that an educated and healthy workforce or the effective rule of law.

While I can recall conversations with clients on this issue going back at least 10 years, you do tend to see the pattern that it becomes a greater concern in times of austerity, high cost of living or other pressures on public spending. It’s therefore likely that interest in tax transparency and responsibility will once again rise in 2022 as a result of significant increases in the cost of living.

Investor interest does tend to spike when there is a high-profile tax dispute in the news and this may lead to concern about how exposed other holdings are and how well investment managers are assessing and managing the associated risks.

There is also a growing expectation for companies to be run in the long-term interests of their stakeholders and tax responsibility is now widely recognized as a key factor in the overall good governance that underpins this approach.

Also, at a very basic level, investors do not like surprises. If a company is exposed to financial or reputational risks because of its more aggressive approach to tax optimization then it makes sense for investors to want to understand what these risks are and whether they are acceptable in the context of overall financial and ESG performance.”

Choosing next steps

There’s another possible explanation why more companies do not fear retaliation from tax authorities. Most companies will take a careful and considered approach before launching a challenge that goes beyond the usual levels of dialogue in a controversy.

For example, among companies open to challenging a tax authority’s position, over half (57%) will only engage in a dispute if they are sure that the case will remain outside the public domain. For those who do choose to challenge through litigation, this is undertaken with an understanding that sometimes only the courts can identify the appropriate treatment on a complex tax point.

“It is true that not always can an agreed solution be reached,” noted Salmerón, “and logically in those cases we are devoted to defend the interest of our group, so that we activate then all legal available paths, including judiciary.”

Clearly this will be a carefully considered decision, and this caution underlines how well businesses understand the reputational impact of tax controversy.

Another vital pre-condition before launching a challenge is a supportive second opinion. Fifty-two percent of survey respondents rely on external advisors before deciding whether to challenge the tax authority’s position. This confirms the trend, discussed below, for organizations to partner with external advisors who already have experience in resolving similar disputes. It is likely that this past experience, as well as the benefit of a fresh pair of eyes looking at an entrenched dispute before choosing to commit to a round of further challenge, is what leads organizations to seek external advice at this point.

Unsurprisingly, the largest companies – those with revenues exceeding $5 billion – are most likely to have created dedicated senior tax dispute roles, with 92% having a VP Tax Controversy or similar. Geographically, meanwhile, the hiring of such staff shows a link to recent experience of disputes.

For instance, 96% of North American companies but only 57% of Latin American ones have experienced more tax disputes at a global level since 2020. And at a global level, 79% of North American organizations have senior management dedicated to tax controversy, versus just 43% in Latin America.

European and Asian companies evidence a similar link, with about 80% of each experiencing more global tax disputes, and just under 70% of each possessing dedicated resources to handle such controversy.

Alongside seniority, experience and specialization are key.

The sometimes high cost associated with hiring specialized staff may explain why companies are far less likely to have dedicated senior staff at domestic level, where many regions are also not reporting more disputes. Only in Europe did a majority (53%) report a rise of tax controversy cases at domestic level, and this region’s companies were also most likely to have dedicated senior staff for their home country, with 78% confirming this.

The outlier is North America, where 75% of companies have dedicated resources at domestic level despite only 10% reporting more disputes in this arena in the last two years. This is likely a reflection of the fact that North America is home to many of the world’s largest companies which, as we have seen, are generally more likely to be ahead of the trend of creating senior tax controversy roles.

Alongside the right people, companies are increasingly recognizing the value of case management tools for their tax disputes. Such systems are proving increasingly valuable, especially in complex, multi-jurisdictional disputes where companies need to manage many processes in parallel.

The use of case management software correlates strongly to a company’s employment of specialized tax controversy staff. North American companies are most likely to have both at the global level, with 81% using tax dispute management tools, while Latin American companies are the least likely to have either.

Europe is the only region where companies, on average, prefer dedicated tax dispute staff and case management software for domestic rather than global operations, again reflecting their greater exposure to disputes at this level.

External support

Even the most experienced in-house teams reach their limits in some disputes. “At Repsol, we are proud of a strong in-house department where we perform an integral handling of tax issues,” said Salmerón. “However, and especially in some key and complex matters, it is always really valuable to trust in technically skilled advisors who can provide different angles and enrich our analysis.”

This view is reflected across the companies surveyed. Over two-thirds of respondents always or usually seek an independent, external view at the appropriate point. Asia-Pacific showed the strongest preference for external advice and North America the weakest, which reflects the latter region’s world-leading commitment to dedicated in-house staff for tax disputes.

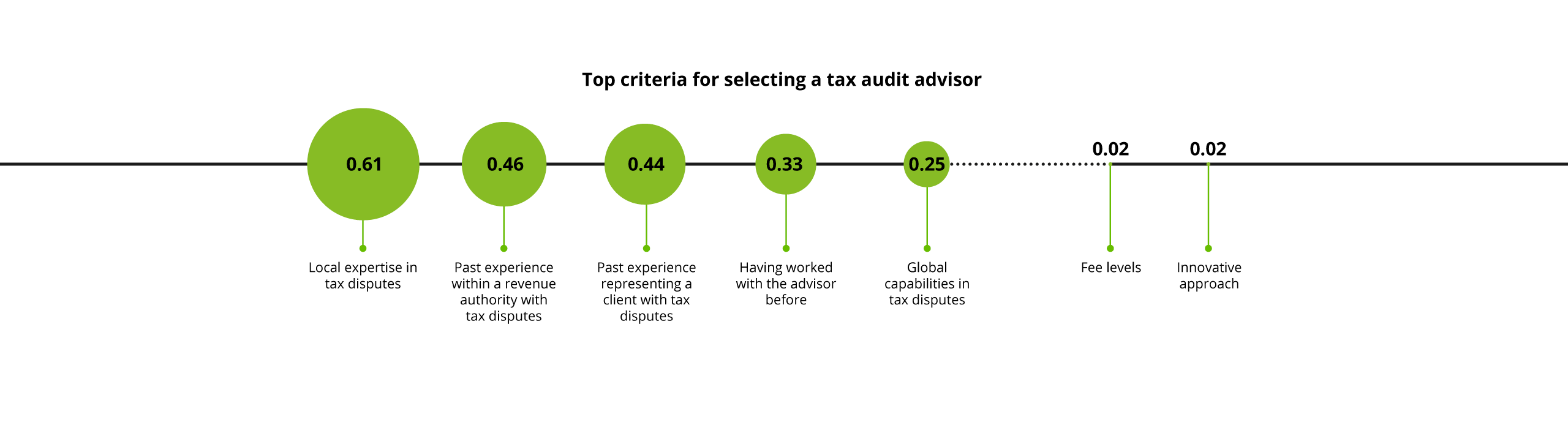

When considering engaging external advisors, companies cited local expertise and prior experience from within a revenue authority as the drivers of any decision to hire external support. Controversy management is a potentially high-risk area, and specialist advisors with a proven track record are the preferred partner for businesses facing disputes. This specialist support clearly supplements the knowledge and experience that the organization has in-house, rather than replicating work, as even large organizations will struggle to retain a permanent, large staff purely to deal with tax controversy matters.

“We have a presence in 30 countries globally. In some countries we do not have resources and especially in these countries we need local advisors,” observed Jäälinoja.

Given this relationship between the business and their external controversy specialists, prior experience of an advisor can be an important factor when businesses hire controversy support, reassuring the organization that its advisor already has a deep understanding of its business.

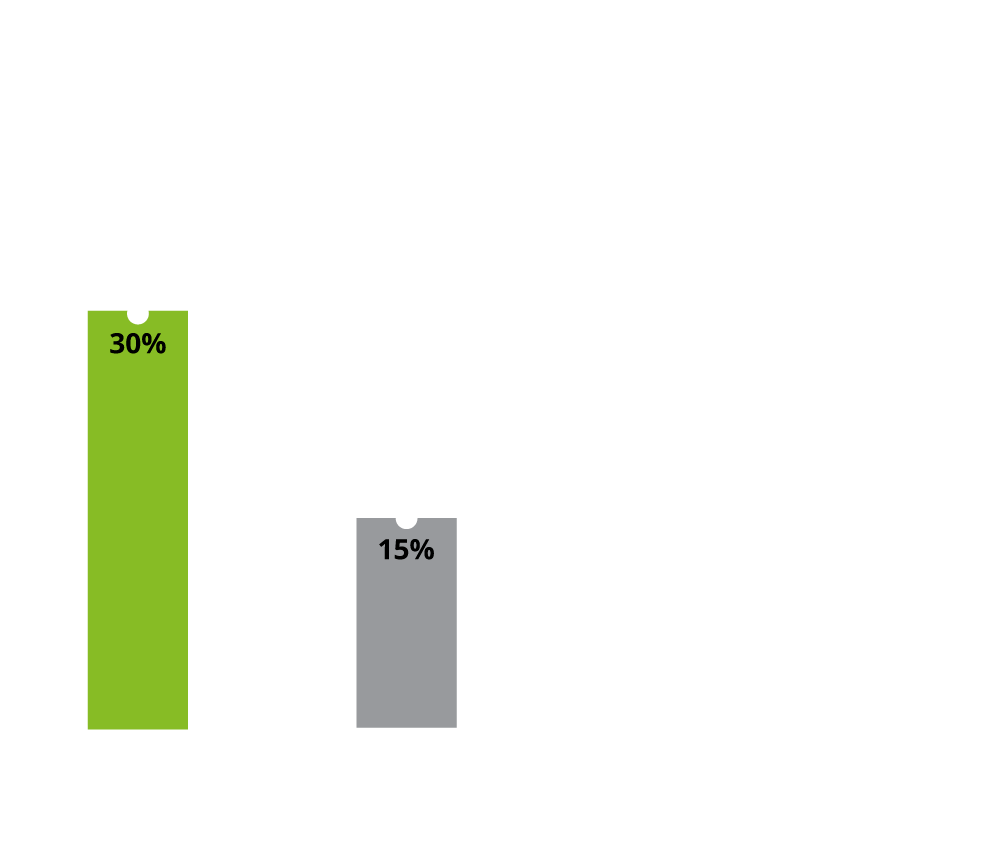

At the same time, given the strategic importance of resolving controversy swiftly and appropriately, the cost of outside advice is not a key consideration. Rather, organizations know that this support is a necessity due to the impact a controversy can have on a business financially and reputationally. This is reflected in the fact that 38% of companies turn to external advisors when a dispute threatens to breach financial or risk thresholds. This is considerably higher than the global finding that 17% of companies engage advisors immediately, a cohort that rises to 28% in Asia-Pacific.

Qureshi, Genpact’s Head of Taxes for Asia-Pacific, said large multinational companies will often outsource: “If you have limited resources within, then you really need to tap into the resources available outside.”

Jäälinoja agreed: “Tax-related compliance and transparency is requiring more and more resources – there is no way around that. At the current stage of uncertainty, flexibility in budget is needed; one cannot fully predict where and when disputes arise and how much external resources are needed.”

Clarity of purpose

Finally, whether using solely in-house resource or a mix of internal and external support to handle a tax controversy, it is important for organizations to be clear what the route to resolution looks like, what a good settlement is and why. Failure to do so can result in both lack of clarity – and therefore delays in reaching resolution – and potentially punitive costs if it’s not possible to reach agreement.

“Any action from the tax authorities, especially if the taxpayer fails at the end of the litigation process, may come with several years of interest and penalties,” commented Qureshi. “Companies are obviously concerned about this.”

While hardly anyone rules out challenging authorities as a matter of principle, companies have criteria to determine what to do when. Some have clear red lines, crossing of which will always trigger a challenge.

Working with external advisors can be helpful in identifying what next steps are appropriate to take and when and how to do so. As such, it’s no surprise that 52% of companies seek external advice before commencing a challenge – a preference shared by companies of all sizes. Involving external parties can also help identify key decision points in a tax controversy by drawing on prior experience with the relevant tax authority and their resolution processes.

The survey results indicate the largest companies (turnover exceeding $5 billion) are twice as likely as businesses with turnovers below $1 billion (18/60 versus 19/123) to hire consultants from the outset of a dispute. Large businesses are also more willing to challenge adjustments. This is likely a result of larger businesses having more established governance and decision-making processes on a range of issues (including controversy), as well as the potentially larger settlements at stake if a dispute cannot be resolved.

And while all our interviewees stressed a preference for avoiding disputes through transparency and ongoing dialogue with authorities, a challenge is sometimes the only option.

“We collaborate as much as possible with the authorities,” said Salmerón. “Having said that, if we are unable to arrive to an agreement, we support and defend the interest of the company.”

Clarity of purpose

Finally, whether using solely in-house resource or a mix of internal and external support to handle a tax controversy, it is important for organizations to be clear what the route to resolution looks like, what a good settlement is and why. Failure to do so can result in both lack of clarity – and therefore delays in reaching resolution – and potentially punitive costs if it’s not possible to reach agreement.

“Any action from the tax authorities, especially if the taxpayer fails at the end of the litigation process, may come with several years of interest and penalties,” commented Qureshi. “Companies are obviously concerned about this.”

While hardly anyone rules out challenging authorities as a matter of principle, companies have criteria to determine what to do when. Some have clear red lines, crossing of which will always trigger a challenge.

Working with external advisors can be helpful in identifying what next steps are appropriate to take and when and how to do so. As such, it’s no surprise that 52% of companies seek external advice before commencing a challenge – a preference shared by companies of all sizes. Involving external parties can also help identify key decision points in a tax controversy by drawing on prior experience with the relevant tax authority and their resolution processes.

The survey results indicate the largest companies (turnover exceeding $5 billion) are twice as likely as businesses with turnovers below $1 billion (18/60 versus 19/123) to hire consultants from the outset of a dispute. Large businesses are also more willing to challenge adjustments. This is likely a result of larger businesses having more established governance and decision-making processes on a range of issues (including controversy), as well as the potentially larger settlements at stake if a dispute cannot be resolved.

And while all our interviewees stressed a preference for avoiding disputes through transparency and ongoing dialogue with authorities, a challenge is sometimes the only option.

“We collaborate as much as possible with the authorities,” said Salmerón. “Having said that, if we are unable to arrive to an agreement, we support and defend the interest of the company.”

Conclusion

Tax controversy levels have risen sharply in recent years and now typically involve multiple jurisdictions on either single or several issues. These disputes are taking longer than before to reach resolution. For the reasons shared above, none of these trends are likely to alter in the near to medium term.

Experience is crucial in resolving controversies efficiently and appropriately, particularly if this includes an understanding of tax authorities’ drivers and governance around settlements. The survey also shows the value that companies place on strong and established relationships with tax authorities.

At a time when many businesses feel they are not able to have dialogue as frequently with tax authorities as they would like during a controversy, it is no surprise that prior work within a revenue authority is a key draw when companies turn to consultants in tax controversy cases.

Preparation is also key. “You can do much to prevent disputes beforehand,” said Outokumpu's Jäälinoja, citing avenues such as advance pricing arrangements or cooperative compliance programmes. She added: “It is also necessary to have processes and controls in place which assure that potential issues, which may be open to different interpretations by the company and different tax administrations, are detected beforehand and tackled.”

This more proactive approach recognizes that prevention is better than cure. It is also a reaction to the fact that these days tax authorities across North America, Asia-Pacific and Europe raise conversations around controversy at an earlier stage than before and sometimes even prior to a controversy being formally opened. It is not surprising, therefore, that businesses increasingly see controversy management as part of standard business processes.

“Having a tax risk framework is key,” said Salmerón. “It sets not only the procedures you follow to avoid problems, but also the level of risk appetites you would like to have.”

Yet even the most cautious and communicative of multinationals will face disputes, sometimes due to truculent authorities and sometimes due to confusion on both sides about the tax code. As such, it is important for companies to embed strong dispute resolution processes within their wider tax governance, and to keep senior management in the loop.

“Should a dispute arise, there must be a process in place to report and handle it appropriately within the company,” observed Jäälinoja.

In summary, this survey shows that companies have responded already to higher levels of tax controversy by hiring dedicated resource in their tax departments with staff assigned to managing and handling controversies.

The businesses who are ‘best in class’ at responding to controversy typically support their in-house teams with a combination of risk and project management tools; the input of external advisors; good communication channels with internal and external stakeholders; and a well-understood decision tree that can be consulted during the controversy settlement process.

Download this report

Appendix

Methodology

This report is based on a survey of 303 tax, finance and legal in-house professionals, conducted by International Tax Review on behalf of Deloitte. Fieldwork took place in February and March 2022. Forty-six percent of respondents are C-level executives with the remainder being vice-presidents, deputy vice-presidents or other senior management.

Thirty percent of respondents are based in the Americas, a further 30% in Europe, and 20% each in the Middle East and Africa, and in Asia-Pacific.

Respondents are also almost evenly spread across all industries and sectors.

Revenues range from less than $500 million to $5 billion plus, also evenly distributed. Lastly, 56% of companies in the sample are publicly listed, with the remainder being privately owned.

In addition to the survey, in-depth interviews were conducted with five corporate leaders. Deloitte and International Tax Review would like to thank the following independent experts for their contributions to this report:

ABOUT DELOITTE TAX SERVICES

Trusted. Transformational. Together.

Digitization of tax, sustainability measures, workforce mobility and other ambiguities on the global tax landscape are fundamentally shifting how the tax function operates. Tax leaders must become strategic advisors while maintaining flawless compliance.

We work with you side-by-side, bringing a rigorous approach to get tax work done accurately, efficiently, and on time. We connect you to expertise, capabilities, technology, and innovative ideas to make you more agile. As you navigate your changing role, we will help you lead your business through complexity with confidence.

ABOUT INTERNATIONAL TAX REVIEW

International Tax Review is the market-leading masthead servicing the international corporate tax payer community, providing an essential source of news, analysis, publications and events for leading tax experts, directors, lawyers and CFOs.

Production

- Managing editor: Ben Bschor

- Writer: Alex Derber

- Report design: Claire Boston

Disclaimer

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited (“DTTL”), its global network of member firms, and their related entities (collectively, the “Deloitte organization”). DTTL (also referred to as “Deloitte Global”) and each of its member firms and related entities are legally separate and independent entities, which cannot obligate or bind each other in respect of third parties. DTTL and each DTTL member firm and related entity is liable only for its own acts and omissions, and not those of each other. DTTL does not provide services to clients. Please see www.deloitte.com/about to learn more.

Deloitte provides industry-leading audit and assurance, tax and legal, consulting, financial advisory, and risk advisory services to nearly 90% of the Fortune Global 500® and thousands of private companies. Our professionals deliver measurable and lasting results that help reinforce public trust in capital markets, enable clients to transform and thrive, and lead the way toward a stronger economy, a more equitable society and a sustainable world. Building on its 175-plus year history, Deloitte spans more than 150 countries and territories. Learn how Deloitte’s more than 345,000 people worldwide make an impact that matters at www.deloitte.com.

This report contains general information only, and none of Deloitte Touche Tohmatsu Limited (“DTTL”), its global network of member firms or their related entities (collectively, the “Deloitte organization”) is, by means of this report, rendering professional advice or services. Before making any decision or taking any action that may affect your finances or your business, you should consult a qualified professional adviser. No representations, warranties or undertakings (express or implied) are given as to the accuracy or completeness of the information in this report, and none of DTTL, its member firms, related entities, employees or agents shall be liable or responsible for any loss or damage whatsoever arising directly or indirectly in connection with any person relying on this report. DTTL and each of its member firms, and their related entities, are legally separate and independent entities.

© 2022. For information, contact Deloitte Global.