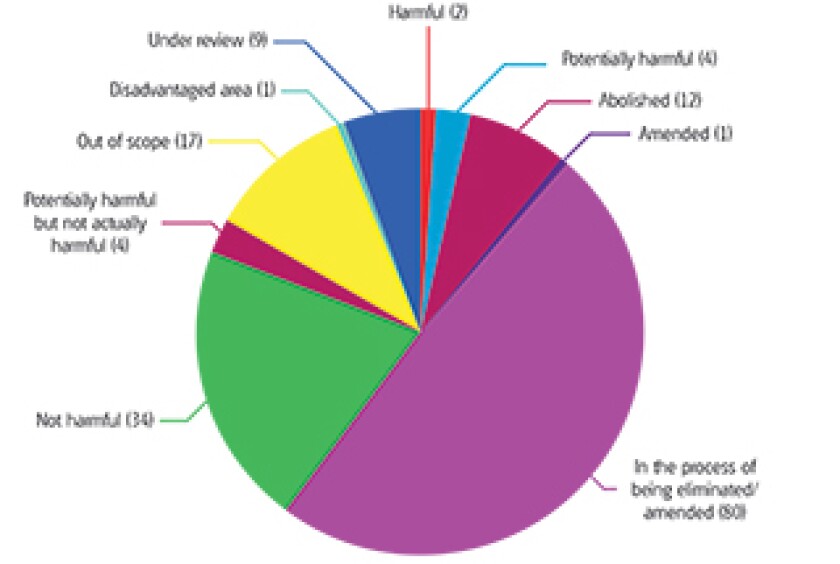

BEPS Action 5 – Countering harmful tax practices more effectively by taking into account transparency and substance is one of the four BEPS minimum standards. To date, 102 jurisdictions have committed to its implementation, and 2017 is a decisive year in translating that commitment into action. Achim Pross, Kevin Shoom and Melissa Dejong of the OECD, discuss the first results of the work under BEPS Action 5, and its significance in achieving the goals of the BEPS project.

Unlock this content.

The content you are trying to view is exclusive to our subscribers.

As tax teams face pressure from complex rules and manual processes, adopting clear ownership, clean data and adaptable technology is essential, writes Russell Gammon, chief innovation officer at Tax Systems

The deal establishes Ryan’s property tax presence in Scotland and expands its ability to serve clients with complex commercial property portfolios across the UK, the firm said

Trump announced he will cut tariffs after India agreed to stop buying Russian oil; in other news, more than 300 delegates gathered at the OECD to discuss VAT fraud prevention

Taxpayers should support the MAP process by sharing accurate information early on and maintaining open communication with the competent authorities, the OECD also said

The Fortune 150 energy multinational is among more than 12 companies participating in the initiative, which ‘helps tax teams put generative AI to work’

The ruling excludes vacation and business development days from service PE calculations and confirms virtual services from abroad don’t count, potentially reshaping compliance for multinationals