Click on the panels above to access content on each of the individual Actions

Pre-2012, the most commonly uttered four-letter word on the International Tax Review writing floor was almost certainly something explicit.

Late submissions of copy, pernickety PR requests at the eleventh hour and inflexible printers all conspired to ensure such a word held the number one spot for years, nay decades. However, that accolade now falls – unequivocally – to the acronym 'BEPS'. There isn't even a close second.

This cleansing of the air in ITR Towers is thanks to a watershed moment which came in the form of the G20 commissioning the Paris-based OECD to kickstart a two-year project that would change the face of international taxation and, by extension, the cleanliness of the ITR editorial staff's vocabulary, forever.

The rise in prominence of international taxation issues is unprecedented, and concepts that were previously confined to the business pages of broadsheet newspapers are now regular front-page fodder for publications of all shapes and sizes. This expansion of stakeholders has brought challenges, but has also brought momentum for change on a level that has not been achieved since the 1920s and the work of the League of Nations.

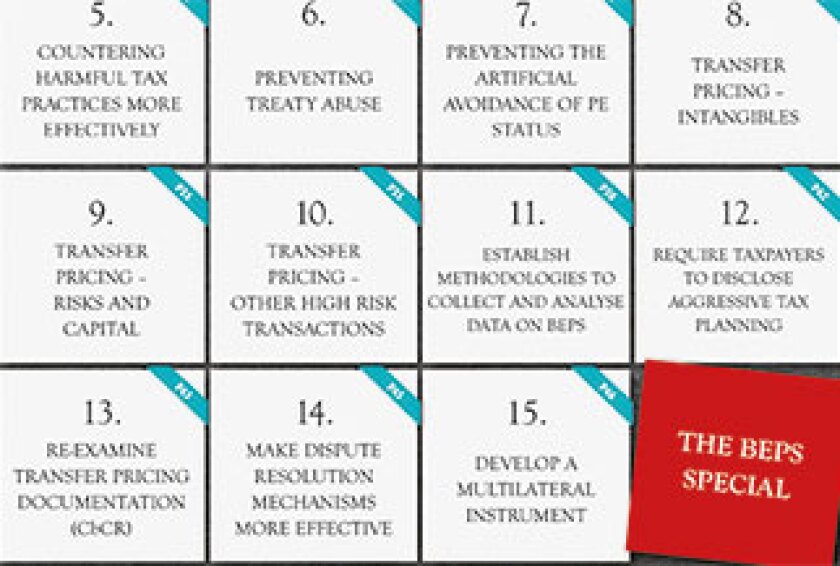

The breadth and depth of work that has gone on in the past two years is clear to see, but it does not stop here. As we enter 2016 – and the implementation phase of BEPS – we hope this BEPS Special provides you with the information and insight you need to prepare for a new era of international tax and a new era for business as a whole.