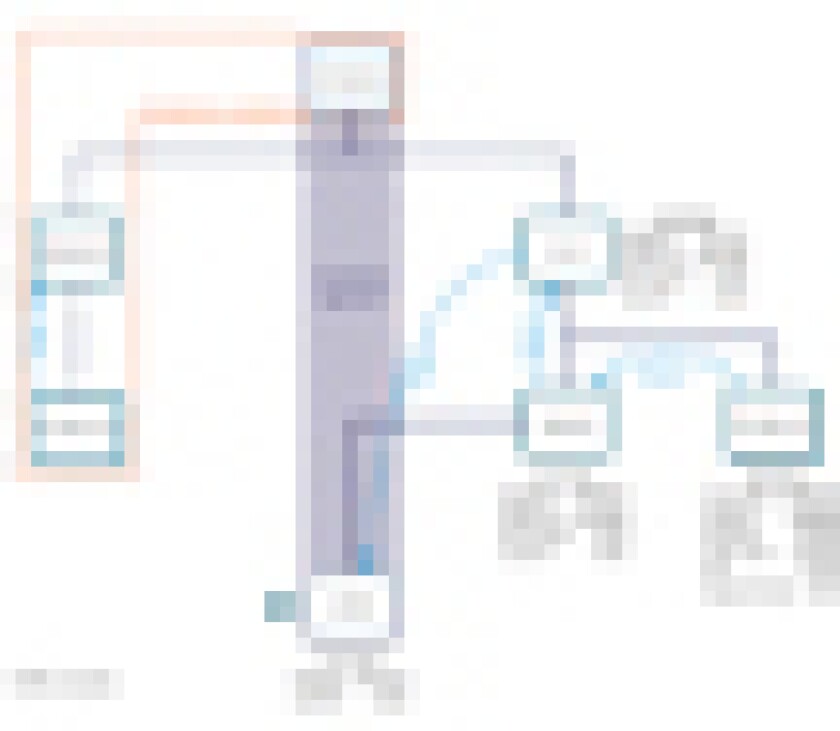

On February 13 2013, the OECD released a report on tax planning by multinationals that reduces group corporate tax liability to an unacceptably low level, as a first step against base erosion and profit-shifting (BEPS). In the preceding months Starbucks, Google and several others were publicly attacked for not paying their “fair” share. Johann Muller, a member of the international corporate taxation department at the Danish Tax Authority – submitting this article in a personal capacity in advance of the OECD Working Party No 6 meeting in March – examines the issues that need to be addressed when looking at examples 1 and 2 to Annex C of the BEPS report.

Unlock this content.

The content you are trying to view is exclusive to our subscribers.

The deal establishes Ryan’s property tax presence in Scotland and expands its ability to serve clients with complex commercial property portfolios across the UK, the firm said

Trump announced he will cut tariffs after India agreed to stop buying Russian oil; in other news, more than 300 delegates gathered at the OECD to discuss VAT fraud prevention

Taxpayers should support the MAP process by sharing accurate information early on and maintaining open communication with the competent authorities, the OECD also said

The Fortune 150 energy multinational is among more than 12 companies participating in the initiative, which ‘helps tax teams put generative AI to work’

The ruling excludes vacation and business development days from service PE calculations and confirms virtual services from abroad don’t count, potentially reshaping compliance for multinationals

User-friendly digital tax filing systems, transformative AI deployment, and the continued proliferation of DSTs will define 2026, writes Ascoria’s Neil Kelley