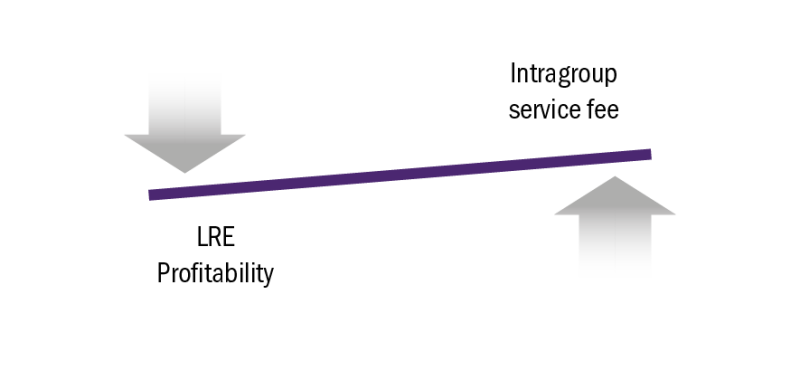

The arm’s-length guaranteed profit of a low-risk entity (LRE) will not alleviate the transfer pricing (TP) exposure of the intragroup services (IGS) fee that is charged to allocate appropriate profit/loss within the group entities based on the value creation concept. The absence of clear guidance in Indonesia on the allocation of excess profits or losses under this scenario may result in the tax authority viewing IGS separately and in isolation from the LRE’s profitability.

LRE, excess profit, and IGS

Limited/low risk structures in the form of low-risk distributors, service providers, or contract manufacturers are common business models adopted by multinational corporations in Indonesia. These low-risk models work in a manner where the LRE performs routine functions and bears limited risks and is accordingly entitled to a stable profit.

|

|

“The arm’s-length guaranteed profit of a low-risk entity will not alleviate the TP exposure of the intragroup services fee that is charged to allocate appropriate profit/loss within the group entities based on the value creation concept.” |

|

|

However, in practice, the LRE is often seen to generate a profit level that is far above routine profits derived from retaining revenue from third party customers, while the significant functions, assets, and risks (FAR) with regard to this revenue are assumed by the global/regional principal or head quarter (HQ) as the value creator. Following the value creation concept, the LRE would rely on the functional comparability analysis to ascertain the arm’s-length profit that it should retain, while the excess profit is allocated to the location/entity where the value is created.

Both OECD Transfer Pricing Guidelines and the UN Transfer Pricing Manual emphasise that excess profit/loss should be allocated to the entity performing important functions, controlling economically significant risks, and contributing assets to create something valuable (critical success factor) for the group. Often, the global or regional principal is referred to as the value creator considering its role as an entity that assumes entrepreneurial risks and owns intangible assets.

Depending on the characteristic of the LRE, among other things, the allocation of this excess profit to the global/regional principal can be done by way of IGS charges, which typically include global/regional service fees and other high value-adding service fees. This form of arrangement is based on the premise that the services and the service provider play a pivotal role in the sustainability/success factor of the LRE’s supply chain and business.

Allocation of excess profit/loss from an Indonesian perspective

In a post-BEPS era, it has been widely accepted that profits should be taxed where economic activities take place and value is created. Indonesian TP regulations have adopted a similar concept since 2013, which requires the alignment of functions and risks with remuneration (DGT Regulation PER-22/PJ/2013). However, the mechanism for performing such alignment in the case of deviation between functions, risks and remuneration has not been spelt out explicitly in the regulation.

While upward profitability adjustment to ensure a stable margin for LRE has rarely been questioned, it is the downward adjustment (i.e. reduction in profitability of the Indonesian entity) that has been an object of intense scrutiny by the local tax office. Therefore, an allocation of excess profit of any kind or forms, including IGS, is likely to attract the attention of the tax office, and be subject to challenge.

Notwithstanding the fact that the Indonesian Directorate General of Taxes (DGT) may consider the arm’s-length profit of the LRE while assessing such arrangement, the DGT is likely to scrutinise the quantum of the IGS in isolation regardless of the profitability of the LRE.

As this relates to services transaction, existence and benefit tests (other than the arm’s-length pricing of the services) are routinely assessed by the DGT based on the prevailing TP regulations in Indonesia (DGT Regulation PER-32/PJ/2011 and PER-22/PJ/2013 and DGT Circular SE-50/PJ/2013) to ascertain whether the IGS transaction can be considered at arm’s-length. On the other hand, the objective of a profit-linked service fee (which is, to align profit allocation in line with value creation) for an LRE differs from the typical standalone IGS transaction. Following this issue, Table 1 discusses some of the aspects that are typically challenged by the DGT in a TP audit.

Table 1 |

|

Matters |

Observations |

Documentation |

The DGT usually requests the taxpayer provide documentation to prove the existence and benefit of the services. Failure to provide sufficient information to substantiate the arm’s-length nature of the allocation of excess profit (which is deemed a service transaction), will result in disallowance of IGS payment as a deduction for corporate income tax purposes by the DGT. |

Expectation that higher fees equal higher profitability |

The DGT usually expects that the high fees paid to the related party should correspond to a high profitability earned by the LRE to show that the services are highly valuable and provide commercial benefit to the LRE. However, the DGT’s expectation might be difficult to satisfy considering the generally stable profit retained by the LRE. |

Cost allocation base |

The DGT usually challenges the cost basis and allocation of the costs to the service recipients and may even demand time-keeping sheets or allocation to account for time spent in providing the service to support the cost allocation base of a typical standalone IGS transaction. The allocation of the cost and the time spent to calculate the IGS charges most likely will not be available since those components are less relevant to the type of high value-adding services provided by the principal. |

Capabilities/credentials of the teams providing the services |

This has been an increasing area of focus for the DGT where the capabilities of the service provider are validated. This element is often assessed through review of the detailed experience, qualification and certification of the resources rendering the service and their expertise in the specific service they are providing. |

The trajectory of the LRE’s performance |

The DGT often takes a hindsight approach to check the trajectory of the LRE in terms of FAR, profitability, and notable changes in the chargeable amount for the IGS. Any significant changes to these elements should entail a solid justification. |

Evaluation of the LRE’s FAR |

There is the possibility that the DGT may reassess the characterisation of the LRE based on the facts and actual condition during the year to evaluate the allocation of excess profit (deemed service) as genuine. The DGT may assume that the LRE might intentionally shift profits through the mischaracterisation of entities. For example, an entity may, during a period of economic upturn, be classified as a limited risk distributor and be rewarded with a stable (but relatively low) margin, when in reality it is fulfilling the role of a fully-fledged distributor and should be sharing in the economic profits earned by the group as a whole. |

What the Indonesian taxpayer can do to be prepared

Substantiate the IGS: With the implementation of BEPS Action 13, the DGT now has access to a group’s financial data. Thus, the DGT can closely assess IGS transactions to ensure that the transactions are not ‘sham’ and not entered into with the ‘primary intention of avoidance of taxes’. Hence taxpayers should be able to accurately capture and prove the value of the IGS, and more specifically the fact that the services are essential for the operations and supply chain, and sustainability of the LRE’s business. Furthermore, taxpayers should be able to justify that the service provider has sufficient nexus to be considered as value creator to warrant the excess profit of the LRE. It is critical to provide a detailed overview of the entire supply chain to allow the IGS to be seen as a critical component of the profit allocation, and not just a standalone transaction. In the absence of a formal regulation to address this situation and without reliable substantiation of the IGS, the LRE may be exposed to high TP risk.

Strong defence file: Taxpayers should prepare a robust defence file consisting of tangible and demonstrable facts that could support the existence, benefit, and the arm’s-length basis of the services. The supporting documents may include, but not be limited to, agreements, overview of the supply chain management, detailed functions/responsibilities of the service provider along with the credentials of the employees rendering the services, email correspondence, minutes of meetings, key reports on the provision of the service, among others.

Harness tax technology: The periodic and regular manual collation of evidence is time consuming and tedious. As such, taxpayers may have to build data frameworks and resort to technology/tools that will enable them to collate appropriate documentation on a real-time basis and in a more time and cost-effective manner.

Regular review of the transaction structure and pricing policy: Taxpayers may need to review the transaction structure and pricing policy regularly to ensure compliance with the latest regulations and to evaluate feedback from the DGT on the ongoing arrangement.

Pursue an advance price agreement (APA): To achieve certainty around TP in these disruptive times, an APA, which is forward-looking and time and cost efficient, could prove to be more useful. An APA may help prevent a painful domestic dispute that requires a comprehensive collation of evidence. In 2020, Indonesia issued an updated APA regulation, whereby it strengthened the overall APA framework making it an even more attractive controversy management tool for taxpayers.

Future development

The level playing field of excess profit/loss allocation for the LRE to be in line with the value creation and arm’s-length principle in Indonesia may have an impact upon the implementation of OECD Pillar One blueprint (under the digital economy project) regarding the safe harbour proposal under Amount B which standardises the remuneration of distributors and marketers (OECD’s Tax Challenges Arising from Digitalisation – Report on Pillar One).

As one of the members of the OECD inclusive framework (IF) on BEPS, Indonesia agreed to implement two pillar solutions, including Amount B under Pillar One. The spirit of Amount B in a nutshell is to provide certainty, both for the DGT and the taxpayer, by standardising the benchmarking sets based on regions.

Upon implementation of Amount B, it is expected that the DGT may have more considerations in making adjustments on related party transaction, including IGS, in return for the standardised profit allocated to Indonesia via Amount B. While the application of this approach indicates that the LRE could no longer earn profit below the standardised margin, at least the recognition of excess profit/loss allocation to the principal may finally come to light.

However, it is pertinent to note that we might still have to wait for the adoption of Amount B in Indonesian regulations considering that the proposal and the implementation mechanics are still being discussed among the IF members.

Click here to read all the chapters from ITR's TP Special Focus

Sandra Suhenda |

|

|---|---|

|

Partner Deloitte Indonesia T: +62 21 5081 8813 Sandra Suhendais a partner in Deloitte Indonesia’s TP practice specialising in TP and international taxes. She has more than 20 years’ experience in Indonesian taxation advisory, compliance and dispute resolutions. Sandra has expertise in TP, tax reviews and due diligence, handling tax audit, assist special tax projects, and represents clients in settling disputes at the Indonesian Tax Office and the Tax Court level, and is involved in APA and MAP cases. Sandra is a licensed tax practitioner in Indonesia and a legal proxy before the Indonesian Tax Court. |

Beatrice Simamora |

|

|---|---|

|

Senior manager Deloitte Indonesia T: +62 21 5081 8928 Beatrice Simamora is a senior manager in Deloitte Indonesia’s TP practice and has almost 10 years’ experience advising clients on TP issues. Beatrice has extensive experience in TP planning, review and documentations, and dispute resolution. She has deep interest in litigation and dispute matters and specialises in handling tax/TP litigation cases, which involve settlement of disputes. Beatrice is also adept at dealing with competent authorities in MAP and APA cases. She is a certified tax court attorney and also a lawyer who has an advocate licence to practice law throughout Indonesia. |

Kartika Sukmatullahi Hasanah |

|

|---|---|

|

Assistant manager Deloitte Indonesia T: +62 21 5081 8818 Kartika Sukmatullahi Hasanah is an assistant manager in Deloitte Indonesia’s TP practice specialising in TP and international taxes. Kartika has been involved in a variety of projects for strategic IP planning, tax planning, tax compliance, due diligence, tax diagnostic review and juridical defence for multinational companies. Kartika’s portfolio of clients ranges from startups to major corporation, in the technology, industrial, commodity, banking and retail industries. She holds a master’s degree in Advanced International Tax Law from Universiteit Leiden (Leiden, Netherlands). |